02 Nov 2022

Market Standards: Trends in Loan Buyback Provisions

Typically, without express permission, the voluntary prepayment and loan assignment provisions of the credit agreement would prohibit loan buybacks by the borrower or its affiliates. However, borrower demand for this allowance gained traction following the financial crisis of 2008, when most debt traded below par and borrowers sought to buy back their own loans at a discount on the secondary market rather than repaying them at par. While some syndicated credit agreements continue to allow for loan buybacks, subject to certain conditions and requirements, these provisions are less common in recent credit agreements.

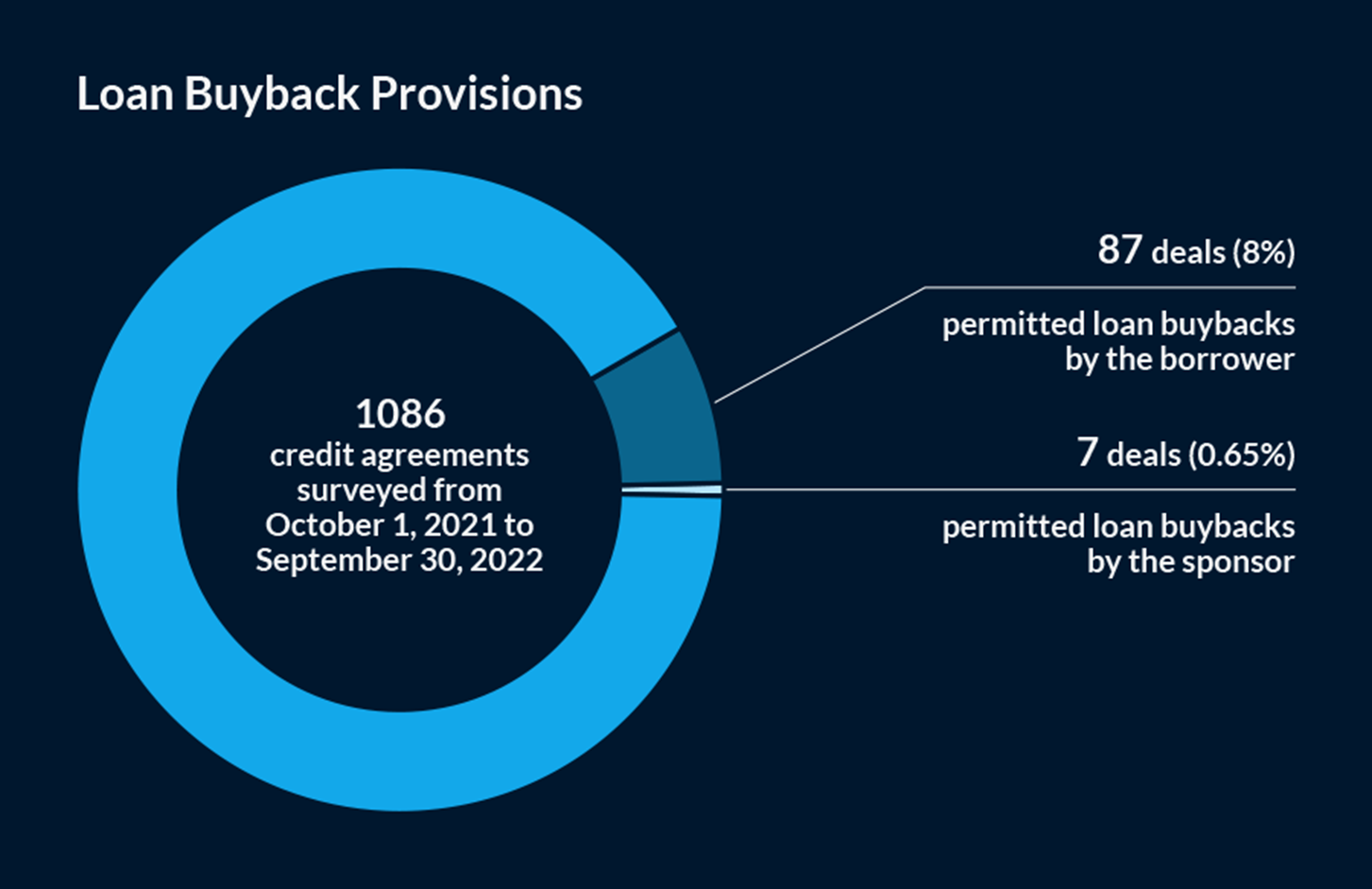

According to Market Standards, out of 1086 credit agreements surveyed from October 1, 2021 to September 30, 2022, only 87 deals (8%) permitted loan buybacks by the borrower (see the search results in Market Standards), and just 7 deals (less than 1%) permitted loan buybacks by the sponsor (see the search results in Market Standards)

{kind=link}

Click here to access credit agreements on Market Standards

Related Content

- Repayment and Prepayment Provisions in Credit Agreements

Read this practice note discussing the prepayment and repayment of loans under a credit facility, whether upon the occurrence of a scheduled payment date or a certain triggering event (such as receipt of excess cash flow or extraordinary receipts, issuance of debt or equity, or an asset sale), voluntarily by the borrower.

- The Client Asks: Can We Pay Down Our Debt?

Review this practice note explaining how you should proceed when a client calls and asks whether the credit agreement permits them to pay off their loans (or buyback notes).

- Borrower Loan Buybacks Clauses (Discounted Voluntary Prepayments) (Credit Agreement)

Use these borrower loan buyback (or discounted voluntary prepayments) clauses in a credit agreement in a syndicated loan transaction to allow the borrower to conduct Dutch auctions to repurchase and cancel their loans in the form of voluntary prepayments.

Practical Guidance Updates

Featuring the latest updates from your Practical Guidance account.

- Market Standards Highlights:

- Cummins Inc. On September 30, 2022, certain subsidiaries of Cummins Inc. (the “Company”) entered into a $1 billion credit agreement (the “Credit Agreement”), consisting of a $400 million revolving credit facility and a $600 million term loan facility made in anticipation of the separation of Company’s filtration business. However, the Credit Agreement will terminate on March 30, 2023 if there is no public sale of shares in the Company’s subsidiary that holds the filtration business. If borrowings become available under the Credit Agreement, the facilities would mature on September 30, 2027. Borrowings under the Credit Agreement would bear interest at varying rates, depending on the type of loan and, in some cases, the rates of designated benchmarks.

Notable Provisions: (1) The Credit Agreement includes a ticking fee ranging from 0.20% (0-44 days after the effective date) up to 0.50% (135-179 days after the effective date). For more information on fees, see Fees in Loan Transactions and Fee Letter Considerations. For template interest rates and fee clauses, see Interest Rates and Fee Clauses (Credit Agreement). (2) In the case of U.S. dollar-denominated loans, adjusted term SOFR includes a 0.10% credit spread adjustment. To track credit spread adjustments, see our Credit Spread Adjustment Tracker. (3) The Credit Agreement includes euro-denominated loans based on EURIBOR. To track loans with interest rates based on foreign benchmark interest rates, see the Foreign Benchmark Rate Loans Tracker.

- Cummins Inc. On September 30, 2022, certain subsidiaries of Cummins Inc. (the “Company”) entered into a $1 billion credit agreement (the “Credit Agreement”), consisting of a $400 million revolving credit facility and a $600 million term loan facility made in anticipation of the separation of Company’s filtration business. However, the Credit Agreement will terminate on March 30, 2023 if there is no public sale of shares in the Company’s subsidiary that holds the filtration business. If borrowings become available under the Credit Agreement, the facilities would mature on September 30, 2027. Borrowings under the Credit Agreement would bear interest at varying rates, depending on the type of loan and, in some cases, the rates of designated benchmarks.

- New Practical Guidance Content

- Market Trends 2022: Benchmark Rate Floor Provisions

- Market Trends 2021/22: Commitment Letter Term Sheet Provisions

- Market Trends 2021/22: Commitment Letters for Acquisition Financing

- Letter of Credit Facilities in Financing Transactions Video

- Representations and Warranties in Credit Agreements Video

- Event of Default Provisions in Credit Agreements Video

- Listen Up! The Practical Guidance Podcast features interviews with industry-leading attorneys on cutting edge issues in the law: NFTs, Cannabis, COVID-19, and more.

- Legal Developments provide the latest updates and analyses of emerging topics impacting your practice area. Visit the Legal Developments page to see the latest topics, which also include breaking legal news and related Practical Guidance content.

- Check out the new Practical Guidance Author Center! Learn about the 1500+ leading attorney authors contributing to our 22 practice areas, and find out how you can Become a Practical Guidance Author.

- Document alerts allow you to stay current on legal developments that affect your practice. Find out how to set up your document alerts.

Experience results today with practical guidance, legal research, and data-driven insights—all in one place.

Experience Lexis+